Healthcare practitioners face unique financial challenges: extended training years, delayed earnings, and the need to balance practice management with long-term wealth building. Selecting the right brokerage services can play a pivotal role in achieving financial independence and retirement readiness. This guide outlines the key differences between advised and non-advised brokerage services, the benefits of incorporating brokerage solutions into your wealth strategy, essential program features to evaluate, and common investment pitfalls to avoid.

Advised vs. Non-Advised Brokerage Services

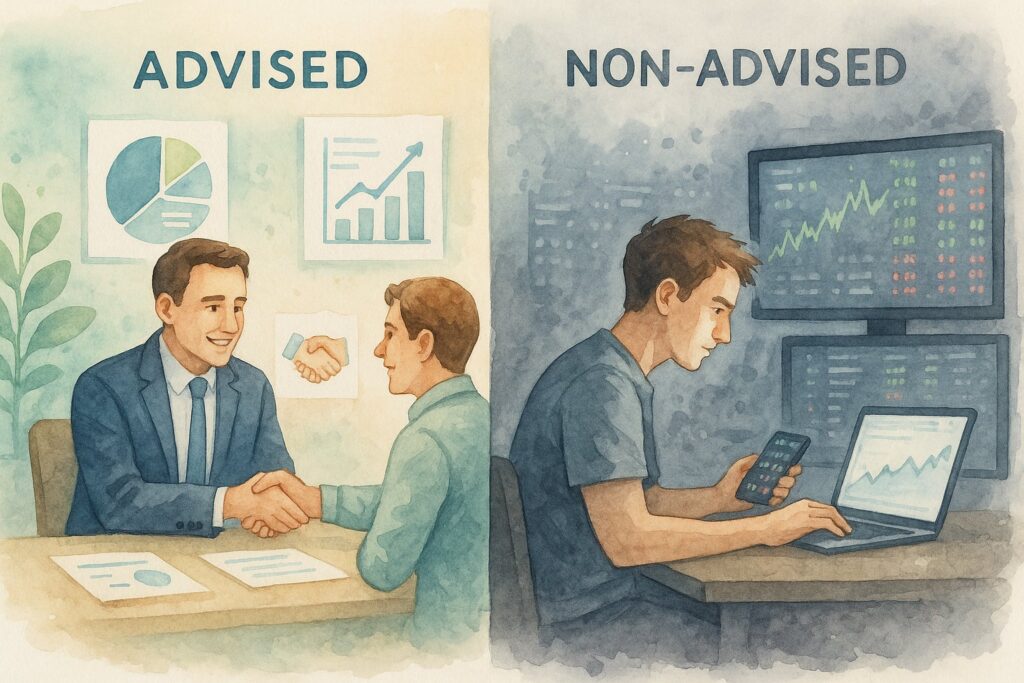

Advised Brokerage Services

- Definition: Investment accounts managed with professional guidance from a licensed financial advisor or advisory firm.

- Key Features: Personalized asset allocation, ongoing monitoring, rebalancing, and tailored recommendations aligned with your goals and risk profile.

- Best For: Practitioners who prefer a structured, hands-off approach and value fiduciary guidance to optimize long-term outcomes.

Non-Advised Brokerage Services

- Definition: Self-directed investment accounts where you select and manage your own securities (stocks, ETFs, mutual funds, bonds, etc.).

- Key Features: Full control over investment decisions, access to trading platforms, and typically lower direct fees.

- Best For: Practitioners who are financially knowledgeable, comfortable making independent investment decisions, and willing to dedicate time to portfolio management.

Key Differences

- Decision-Making: Advisor-driven vs. self-directed.

- Support: Professional guidance vs. independent research.

- Time Commitment: Minimal for advised accounts vs. significant for non-advised accounts.

- Cost Structure: Advisory fees vs. transaction costs or platform fees.

Benefits of Adding Brokerage Solutions to Your Wealth-Building Strategy

- Diversification Beyond Retirement Accounts – Brokerage accounts allow investment flexibility outside of employer-sponsored retirement plans.

- Liquidity and Accessibility – Unlike retirement accounts, brokerage assets can be accessed without early withdrawal penalties.

- Tax Planning Opportunities – Brokerage accounts enable tax-loss harvesting, capital gains planning, and strategic asset location.

- Customized Investment Options – Broader access to ETFs, equities, fixed income, and alternative strategies.

- Wealth Accumulation Across Career Stages – Supports both early-career wealth building and later-stage retirement income planning.

Key Program Features to Look For

When evaluating brokerage solutions, healthcare practitioners should consider:

- Fiduciary Oversight – Ensure advisors are legally obligated to act in your best interest.

- Transparent Fee Structure – Look for clear disclosure of advisory fees, trading costs, and account charges.

- Investment Philosophy – Evidence-based, diversified strategies aligned with your risk tolerance and goals.

- Technology and Reporting – User-friendly platforms with real-time account access, performance reporting, and tax documentation.

- Integration with Financial Planning – Ability to coordinate brokerage accounts with retirement plans, insurance, and estate planning.

- Ongoing Support – Access to advisors for periodic reviews, rebalancing, and adjustments as your career evolves.

Common Investment Mistakes to Avoid

- Overconcentration – Relying too heavily on a single stock, sector, or asset class.

- Market Timing – Attempting to predict short-term market movements, which often leads to underperformance.

- Neglecting Tax Efficiency – Overlooking strategies such as tax-loss harvesting or asset location.

- Ignoring Fees – Small differences in fees compound significantly over time.

- Lack of Rebalancing – Allowing portfolios to drift away from target allocations, increasing risk exposure.

- Emotional Decision-Making – Reacting to market volatility rather than adhering to a disciplined, long-term plan.

Frequently Asked Questions (FAQs)

1. What is the difference between advised and non-advised brokerage services?

Advised brokerage services provide professional portfolio management and ongoing guidance from a licensed advisor, while non-advised services are self-directed accounts where you make all investment decisions independently.

2. Why should healthcare practitioners consider brokerage solutions in addition to retirement accounts?

Brokerage accounts offer flexibility, liquidity, and tax-planning opportunities that complement traditional retirement savings. They can help you diversify beyond employer-sponsored plans and tailor investments to your specific goals.

3. Are advised brokerage services more expensive than self-directed accounts?

Typically, yes. Advised accounts include an advisory fee for professional guidance, while self-directed accounts mainly incur trading costs or platform fees. However, many practitioners find that professional oversight helps them avoid costly mistakes and achieve better long-term outcomes.

4. How do I know if I should choose advised or non-advised services?

If you prefer expert guidance, have limited time, or want a structured, evidence-based approach, advised services may be more appropriate. If you are confident in your investment knowledge and comfortable managing your own portfolio, a non-advised account may suit you.

5. What types of investments can I access through a brokerage account?

Most brokerage accounts provide access to a wide range of investments, including ETFs, mutual funds, stocks, bonds, and in some cases, alternative strategies.

6. What features should I look for in a brokerage program?

Key features include fiduciary oversight, transparent fee structures, a sound investment philosophy, robust technology and reporting tools, integration with financial planning, and ongoing support.

7. What are the risks of managing my own brokerage account?

Common risks include overconcentration in certain assets, emotional decision-making during market volatility, neglecting tax efficiency, and failing to rebalance portfolios regularly.

8. How often should I review my brokerage account?

At a minimum, accounts should be reviewed annually. However, significant life events—such as practice changes, family milestones, or nearing retirement—may warrant more frequent reviews.

9. Can brokerage accounts help with tax planning?

Yes. Brokerage accounts can be structured to take advantage of tax-loss harvesting, capital gains planning, and strategic asset location to improve after-tax returns.

10. How do brokerage solutions fit into my overall financial plan as a healthcare practitioner?

They serve as a flexible complement to retirement accounts, providing additional diversification, liquidity, and tax efficiency. When coordinated with retirement planning, insurance, and estate strategies, brokerage accounts can strengthen your overall financial foundation.

Conclusion

For healthcare practitioners, brokerage services—whether advised or non-advised—can be powerful tools for building and preserving wealth. The right approach depends on your financial knowledge, time availability, and desire for professional guidance. By incorporating brokerage solutions thoughtfully and avoiding common mistakes, you can create a more resilient, tax-efficient, and goal-oriented investment strategy that supports both your practice and your long-term financial independence.

Getting Started: SUBMIT INQUIRY