Navigating your nursing career often means balancing demanding shifts with long-term financial goals. Whether you’re just starting out, building stability in mid-career, or preparing for retirement, brokerage services can play a practical role in helping you manage money, grow investments, and plan for the future. Brokerage services support nurses at every stage by aligning financial strategies with career milestones and personal priorities.

As an entry-level nurse, you may focus on building savings and learning how to invest with smaller amounts. Mid-career often brings higher earnings and the need to balance family, home ownership, or advanced education with long-term financial growth. Retirement planning shifts the focus toward preserving wealth, managing withdrawals, and ensuring income stability.

Brokerage services can fit into each stage differently, whether through advised options that offer professional guidance or non-advised platforms that give you more control. Understanding how these choices line up with your goals helps you make informed decisions that match both your career stage and financial needs.

Understanding Brokerage Services for Nurses

You can use brokerage services to manage investments, build savings strategies, and plan for long-term financial security. These services range from self-directed platforms to full-service advisory models, giving you flexibility depending on your career stage, financial knowledge, and goals.

What Are Brokerage Services?

Brokerage services connect you with financial markets so you can buy and sell investments such as stocks, bonds, mutual funds, and exchange-traded funds (ETFs). A brokerage firm acts as the intermediary, ensuring your trades are executed accurately and securely.

You have the option to manage your own investments or work with an advisor who provides guidance. Self-directed accounts give you control, while advised accounts include professional support for portfolio management and financial planning.

Brokerage services also include account features like retirement accounts (IRAs), taxable investment accounts, and custodial accounts. These options allow you to align your investments with both short-term needs and long-term goals.

Types of Brokerage Services Available

You can choose from different types of brokerage services depending on how much guidance you want.

- Full-Service Brokerage: Offers personalized advice, retirement planning, and portfolio management. Best if you prefer professional support.

- Discount Brokerage: Provides lower-cost trading with fewer advisory services. Suitable if you want to manage investments independently.

- Online Brokerage Platforms: Digital-first services with research tools, mobile apps, and low fees. Good for tech-savvy investors.

- Robo-Advisors: Automated platforms that create and manage portfolios using algorithms. Useful if you want a hands-off approach with lower costs.

Each service type has different fee structures. Full-service firms often charge higher fees, while online and robo-advisors usually have lower costs but less human interaction.

Benefits of Brokerage Services for Healthcare Professionals

Brokerage services can help you address financial needs that are common in healthcare careers. You may face student loan debt early on, irregular work schedules, and the need for long-term retirement planning.

With a brokerage account, you can set up automatic contributions, diversify your investments, and adjust strategies as your income and responsibilities change. This flexibility supports both short-term financial stability and long-term growth.

Advised services may also provide tailored planning for healthcare-specific challenges, such as balancing retirement savings with continuing education costs or preparing for career transitions. Having access to professional guidance can reduce financial stress and help you stay focused on your career.

Financial Needs of Entry-Level Nurses

At the start of your career, your financial priorities often revolve around managing student debt, covering living expenses, and building a foundation for future stability. You benefit from strategies that balance short-term needs with long-term financial growth.

Budgeting and Saving Strategies

Your first step is to establish a clear budget that tracks income and expenses. Nursing salaries vary by region and role, so knowing your exact monthly take-home pay helps you plan realistically.

Break expenses into categories such as housing, transportation, food, debt repayment, and savings. Aim to set aside at least 10–15% of your income for savings, even if it feels small at first.

Consider building an emergency fund equal to three months of living costs. This fund protects you from unexpected expenses like car repairs or medical bills.

If you have student loans, use repayment programs designed for healthcare workers, such as Public Service Loan Forgiveness (PSLF), which may reduce long-term costs if you work in qualifying facilities.

Building an Investment Portfolio

Once you have a budget and emergency fund, you can begin investing. At this stage, your focus should be on low-cost, diversified options that don’t require large starting amounts.

Employer-sponsored retirement plans, such as a 403(b) or 401(k), are often available in healthcare settings. Contribute enough to receive any employer match, since this is essentially free money.

If you want more flexibility, consider opening an Individual Retirement Account (IRA). A Roth IRA can be useful early in your career because contributions grow tax-free, and your current tax rate is likely lower than it will be later.

Keep your portfolio simple with index funds or target-date funds. These options spread risk across many investments and require minimal ongoing management.

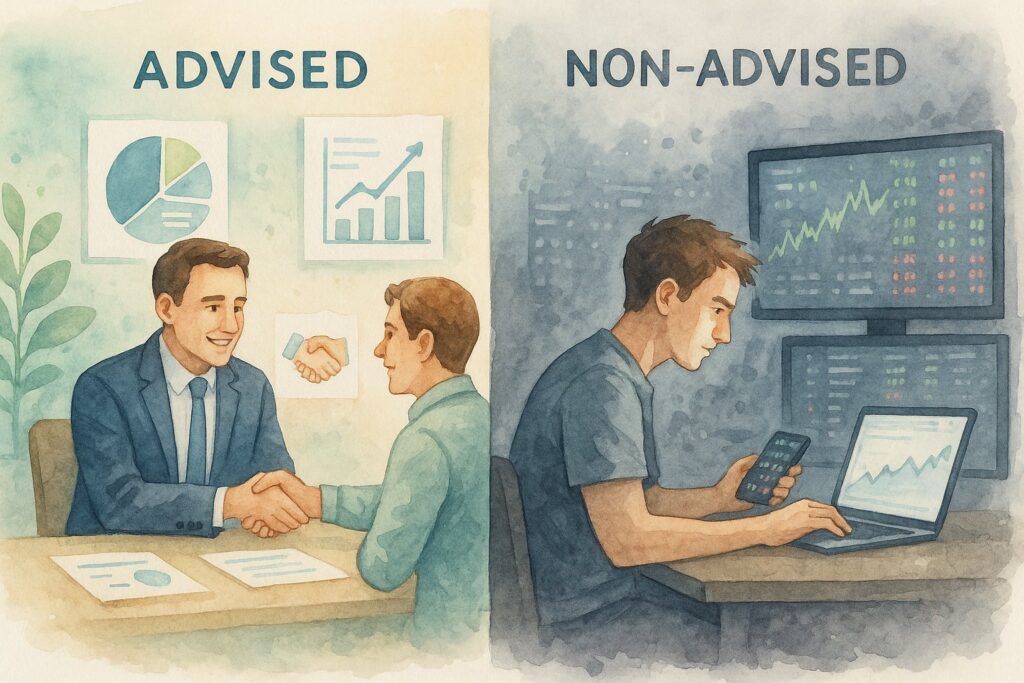

Accessing Advised vs. Non-Advised Brokerage Accounts

When opening a brokerage account, you can choose between advised and non-advised options. An advised account provides professional guidance, which may be helpful if you feel uncertain about investing or want tailored recommendations.

A non-advised account gives you full control at lower cost but requires you to research and select investments yourself. This works well if you prefer independence and are comfortable learning investment basics.

Some firms offer hybrid services, such as robo-advisors, which use algorithms to manage your portfolio at a lower fee than traditional advisors. These can be a good fit if you want guidance without high costs.

Evaluate fees, account minimums, and available tools before deciding which approach fits your financial situation.

Supporting Mid-Career Nurses Through Brokerage Services

At this stage, you often balance higher earnings with greater financial responsibilities. Brokerage services can help you build long-term wealth, protect against risks, and prepare for future expenses with structured strategies that fit your career and personal goals.

Wealth Accumulation Strategies

As a mid-career nurse, your income is usually more stable than in earlier years, which allows you to focus on systematic growth. Brokerage accounts give you access to retirement plans, taxable investment accounts, and automatic contribution options that help you steadily increase savings.

You can use tools such as dollar-cost averaging to invest regularly, regardless of market fluctuations. This approach helps reduce emotional decision-making and smooths out the impact of short-term volatility.

Brokerage platforms also provide access to managed portfolios if you prefer professional oversight, or self-directed accounts if you want more control. Matching your investment style with your available time and comfort level ensures you stay consistent with your goals.

Diversifying Investments

Diversification becomes more important as your assets grow. Instead of concentrating wealth in one account or asset type, you can spread investments across stocks, bonds, mutual funds, ETFs, and real estate investment trusts (REITs).

A brokerage account allows you to build a balanced mix that aligns with your risk tolerance. For example:

| Asset Type | Potential Role |

|---|---|

| Stocks | Growth over time |

| Bonds | Income and stability |

| ETFs/Mutual Funds | Broad market exposure |

| REITs | Real estate diversification |

You may also consider sector diversification, such as healthcare, technology, or energy, to reduce reliance on a single industry. A broker can provide research tools and model portfolios to guide your allocation decisions.

Tax Planning Considerations

Taxes can significantly affect your long-term returns. Brokerage services help you manage this through account selection and investment strategies. For instance, using a mix of tax-advantaged accounts (401(k), IRA, HSA) alongside taxable brokerage accounts allows you to optimize both growth and flexibility.

You can also apply tax-loss harvesting strategies, where you offset investment gains with losses to reduce taxable income. Some platforms provide automated tools for this, while others require manual management.

Paying attention to dividend taxation, capital gains timing, and contribution limits ensures you keep more of what you earn. A broker can guide you on structuring accounts to minimize unnecessary tax burdens while staying compliant with regulations.

Retirement Planning for Nurses Using Brokerage Services

You can use brokerage services to simplify retirement planning by organizing investments, accessing tax-advantaged accounts, and managing risks as your career winds down. These tools help you prepare for the transition out of nursing, optimize savings vehicles, and create reliable income streams after leaving the workforce.

Preparing for Retirement Transition

As retirement approaches, you need to evaluate your financial readiness. A brokerage account allows you to consolidate assets from employer-sponsored plans, such as 401(k)s, and roll them into an IRA for easier management. This step reduces administrative complexity and provides a broader range of investment choices.

You should also review your projected expenses. Healthcare, housing, and long-term care often make up the largest costs. Many nurses underestimate these expenses, so using a brokerage platform to model different spending scenarios can clarify whether your savings align with your needs.

Professional advice can add value during this stage. An advisor connected to a brokerage can help you balance lifestyle goals with financial constraints, while a self-directed approach may suit you if you prefer managing investments independently.

Maximizing Retirement Account Options

Brokerage services give you access to multiple retirement accounts, each with specific advantages. For example:

- Traditional IRA: Contributions may be tax-deductible, but withdrawals are taxed.

- Roth IRA: Contributions are after-tax, but qualified withdrawals are tax-free.

- Brokerage-managed 401(k) rollovers: Consolidates old employer accounts into one place.

You can use these accounts to diversify investments across stocks, bonds, and mutual funds. Diversification reduces reliance on a single source of income and helps manage market volatility.

Catch-up contributions are another benefit once you reach age 50. A brokerage platform makes it easier to increase contributions and track progress toward retirement targets. If you travel or change employers frequently, rolling accounts into one brokerage helps you stay organized and avoid losing track of smaller balances.

Managing Risk and Income in Retirement

Once you retire, your focus shifts from saving to generating stable income. Brokerage services offer tools like systematic withdrawal plans, dividend-paying investments, and bond ladders to create predictable cash flow. These strategies help you cover essential expenses without relying solely on Social Security.

Risk management becomes critical. You may need to reduce exposure to high-volatility assets and increase allocations to more stable investments. A brokerage account allows you to adjust allocations easily and monitor performance.

You can also consider annuities or managed payout funds available through some brokerages. These options provide structured income, though they require careful evaluation of fees and flexibility. Balancing growth with preservation ensures your savings last throughout retirement.

Choosing Between Advised and Non-Advised Brokerage Options

Your financial decisions as a nurse can look different depending on whether you prefer professional guidance or prefer to manage investments yourself. Each approach offers distinct advantages and trade-offs that affect cost, control, and long-term outcomes.

Pros and Cons of Advised Brokerage

With an advised brokerage, you work directly with a financial professional who provides tailored recommendations. This can be especially useful if you have limited time to research investments or want help aligning financial goals with your career stage.

Pros:

- Professional guidance on asset allocation and retirement planning

- Access to research tools and curated investment strategies

- Ongoing support during career transitions, such as moving from staff nurse to advanced practice roles

Cons:

- Higher fees, often through commissions or management charges

- Less flexibility if you prefer to make independent decisions

- Risk of advice being influenced by firm incentives rather than your priorities

For entry-level nurses, the structure can reduce stress and provide a clearer financial path. For mid-career or nearing retirement, the expertise can help manage more complex portfolios.

Pros and Cons of Non-Advised Brokerage

Non-advised brokerage accounts give you full control over your investments. You select, buy, and sell assets without professional input. This appeals to those comfortable with financial research and decision-making.

Pros:

- Lower costs compared to advised services

- Full autonomy over investment choices

- Wide range of investment products without restrictions

Cons:

- Requires time to monitor markets and adjust strategies

- No personalized advice for retirement or tax planning

- Greater risk of mistakes if you lack experience

If you enjoy learning about investments and want to minimize fees, this option may fit. However, it can be challenging during busy nursing schedules or when planning for long-term needs.

When to Transition Between Service Types

You may find that your needs change over time. Early in your career, advised services can provide structure while you focus on building clinical skills.

As your income grows, you might shift to a non-advised model to reduce costs and take more control. Later, as retirement approaches, returning to advised brokerage can help with complex planning such as pension integration, healthcare costs, and withdrawal strategies.

A hybrid approach is also possible. For example, you could manage a portion of your portfolio independently while keeping retirement accounts under professional supervision. This balance allows flexibility while still benefiting from expert input when needed.

Frequently Asked Questions

Brokerage services can help you at different points in your nursing career by offering tools for saving, investing, and planning. Your choices may shift as you move from building savings to managing larger portfolios and preparing for retirement income.

What are the best brokerage services for entry-level nurses to start investing?

You may benefit from brokerages that offer low-cost index funds, no account minimums, and automatic contribution features. Platforms with simple mobile apps and educational tools can make it easier to start investing while managing student loans or entry-level salaries.

How can mid-career nurses benefit from financial planning services?

At this stage, you often have higher earnings and more complex financial needs. Financial planning services can help you balance mortgage payments, family expenses, and retirement contributions while fine-tuning your investment strategy for growth.

What retirement planning advice is available for nurses approaching retirement?

As you near retirement, you need to focus on income stability, tax-efficient withdrawals, and Social Security timing. Brokerages with retirement specialists can help you create a distribution strategy that matches your lifestyle and healthcare needs.

How does a managed brokerage account differ from self-directed investing for nurses?

A managed account assigns professionals to select and rebalance your investments for a fee. With self-directed investing, you choose and manage your own investments, which gives you more control but requires more time and knowledge.

What are the key considerations for nurses when choosing a retirement savings plan?

You should compare employer-sponsored options like 401(k) or 403(b) plans with individual retirement accounts (IRAs). Pay attention to employer match opportunities, contribution limits, and investment choices to maximize long-term growth.

How can nurses maximize their pension benefits upon retirement?

You can maximize benefits by understanding your plan’s payout options, such as lump sum versus annuity payments. Coordinating pension income with Social Security and other retirement accounts can also help you maintain steady income and reduce tax burdens.

Need Help? SUBMIT INQUIRY