As healthcare professionals seek to diversify their retirement portfolios beyond traditional stocks and bonds, alternative investments have gained prominence. Historically, access to private markets—such as private credit, real estate, and infrastructure—was limited to institutional investors and ultra-high-net-worth individuals. However, recent regulatory developments and the evolution of ’40 Act fund structures have opened new pathways for individual retirement accounts (IRAs) to gain exposure to these asset classes.

This whitepaper explores the current regulatory environment, the mechanics of including alternative investments in retirement accounts, and the practical considerations for healthcare professionals evaluating these opportunities.

1. The Growing Demand for Alternatives in Retirement Portfolios

Healthcare professionals often face unique financial dynamics: high income potential, delayed career earnings, and a need for long-term wealth preservation. Traditional retirement portfolios—composed primarily of equities and fixed income—may not fully address these investors’ goals for diversification and inflation resilience.

Alternative investments, including private credit, private real estate, and infrastructure, offer:

- Diversification benefits through low correlation with public markets.

- Potential for enhanced risk-adjusted returns via illiquidity and complexity premiums.

- Income generation from underlying private assets.

Until recently, these opportunities were largely inaccessible within tax-advantaged retirement accounts. Regulatory shifts and innovative fund structures are now changing that landscape.

2. Understanding the Regulatory Framework

2.1. ’40 Act Closed-End Funds

Funds registered under the Investment Company Act of 1940 (the “’40 Act”)—including interval funds, tender-offer funds, and evergreen funds—are designed to provide investors with exposure to less liquid asset classes while maintaining SEC oversight, audited reporting, and periodic liquidity windows.

These structures can generally be held within IRAs and other qualified accounts, offering a compliant pathway to private market exposure without the administrative complexities of direct private placements.

2.2. Self-Directed IRAs (SDIRAs)

Self-directed IRAs allow investors to hold nontraditional assets such as private equity, private credit, and real estate directly. However, SDIRAs introduce:

- Custodial complexity (specialized custodians required).

- Potential for prohibited transactions under IRS rules.

- Valuation and reporting challenges for illiquid assets.

For busy healthcare professionals, these operational burdens often outweigh the benefits unless managed through a trusted advisor or institutional platform.

2.3. ERISA and Employer-Sponsored Plans

The Employee Retirement Income Security Act (ERISA) governs employer-sponsored retirement plans. The Department of Labor (DOL) has issued evolving guidance on the inclusion of private market investments in defined contribution plans. While the DOL has not prohibited such allocations, it emphasizes fiduciary responsibility, transparency, and participant understanding.

3. Key Regulatory Developments

3.1. Department of Labor Guidance

In recent years, the DOL has clarified that fiduciaries of defined contribution plans may include private equity or alternative assets as part of diversified investment options—provided they are structured appropriately and disclosed transparently. This guidance has paved the way for broader consideration of alternatives in retirement contexts.

3.2. SEC Oversight and Disclosure

The SEC continues to refine rules around valuation, liquidity management, and investor protection for semi-liquid funds. Proposed “safeguarding” rules aim to enhance custodial standards and ensure accurate valuation of private assets held in pooled vehicles.

3.3. Implications for IRA Investors

Together, these developments support a growing trend: the institutionalization of private market access through regulated vehicles suitable for retirement accounts. Interval and tender-offer funds, in particular, have become preferred structures for investors seeking compliance and liquidity balance.

3.4. Our Solution for Healthcare Practitioners

The IRS/DOL Regulatory framework for allowing alternatives in retirement accounts may seem daunting. However, healthcare practitioners seeking exposure to private markets in their retirement accounts would greatly benefit from our partnership with Equity Trust.

Cognis Retirement Group partners with EquityTrust through their WEALTHBRIDGE platform. The solution simplifies compliance with existing IRS/DOL regulations; streamlines the opening, funding, and management of your account (s); and complies with reporting requirements on your IRA and or Solo-401K investments in private markets.

Equity Trust’s Universal IRA and Solo-401(k) are both self-directed retirement accounts that allow for investment in a wide variety of alternative and traditional assets. The Universal IRA integrates both types of assets into a single IRA account for simplified management, while the Solo-401(k) is specifically designed for self-employed individuals and their spouses and has higher contribution limits.

| EEQuity Trust’s Universal IRA | Equity Trust’s Solo-401(k) |

| What It Is: A self-directed Individual Retirement Account (IRA) that allows you to hold traditional and alternative investments within the same account. Purpose: To provide a single account for both traditional (stocks, bonds) and alternative assets (real estate, private equity, cryptocurrency). Benefit: Simplifies portfolio management by consolidating different asset types under one login, eliminating the need to manage accounts at multiple companies. Structure: An IRA account that is managed through Equity Trust’s platform. | What It Is: A retirement plan designed for self-employed individuals, small business owners, and their spouses. Purpose: To provide self-employed individuals and small business owners who want to take advantage of higher contribution limits and have the flexibility to invest in alternative assets. Benefit: Simplifies portfolio management by consolidating different asset types under one login, eliminating the need to manage accounts at multiple companies. Structure: A Solo-401(K) account that is managed through Equity Trust’s platform. |

Please speak with one of our advisors for guidance on how to get started:

SCHEDULE FREE MEETING or SUBMIT INQUIRY

4. Opportunities for Healthcare Professionals

4.1. Diversification and Risk Management

For physicians and other healthcare professionals, alternative investments can help reduce portfolio volatility and provide exposure to real assets that may perform differently from public equities during market downturns.

4.2. Access Through ’40 Act Funds

Interval and tender-offer funds offer:

- Quarterly or semi-annual liquidity through redemption windows.

- Simplified tax reporting (Form 1099 rather than K-1s).

- Institutional-grade management with SEC oversight.

These features make them well-suited for inclusion in IRAs, where long-term horizons align with the semi-liquid nature of the underlying assets.

4.3. Potential Return Enhancement

Private market assets often deliver illiquidity premiums—additional returns earned for accepting limited liquidity. Within a retirement account, where funds are typically held for decades, this tradeoff can be advantageous.

5. Risks and Considerations

5.1. Liquidity Limitations

Redemption restrictions mean investors cannot access capital on demand. Allocations should be sized appropriately relative to liquidity needs.

5.2. Valuation and Transparency

Illiquid assets rely on periodic appraisal-based valuations, which can differ from market prices. Understanding the fund’s valuation methodology is critical.

5.3. Tax Implications

While IRAs are tax-advantaged, certain private investments can trigger Unrelated Business Taxable Income (UBTI) if structured improperly. Investors should confirm fund eligibility with their custodian or tax advisor.

5.4. Operational Complexity

Self-directed structures require careful administration and may involve higher custodial fees or reporting requirements.

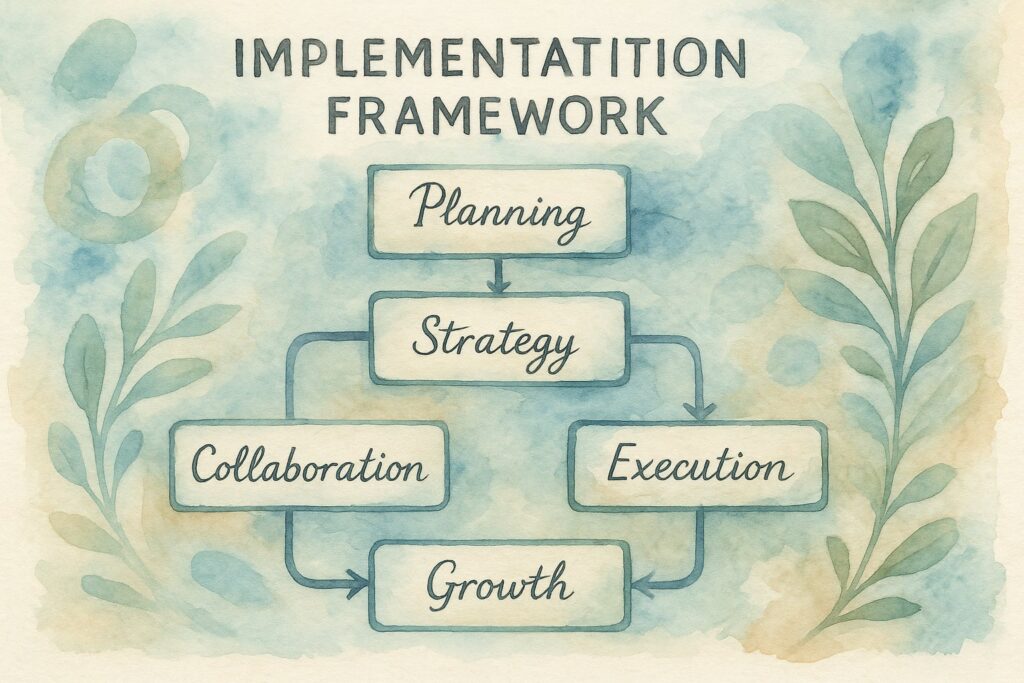

6. Implementation Framework

Step 1: Define Objectives

Clarify whether the goal is income generation, diversification, or long-term growth. Align allocations with the investor’s career stage and retirement timeline.

Step 2: Evaluate Fund Structure

Compare ’40 Act interval funds with direct private placements. Assess liquidity, fees, and transparency.

Step 3: Conduct Due Diligence

Review fund documentation, manager experience, underlying asset strategy, and historical performance.

Step 4: Work with a Fiduciary Advisor

Engage advisors experienced in healthcare financial planning and alternative investments to ensure compliance and suitability.

Step 5: Monitor and Reassess

Track performance relative to objectives, ensuring the allocation remains aligned with changing regulations and personal financial goals.

7. The Road Ahead

The convergence of regulatory evolution, investor demand, and fund innovation is expanding access to private markets within retirement accounts. For healthcare professionals with long-term investment horizons, this shift presents an opportunity to enhance portfolio resilience and potential returns—provided due diligence and regulatory awareness remain central to the process.

As the SEC and DOL continue refining the rules governing alternative investments, investors should stay informed and consult qualified professionals before making allocation decisions.

Call to Action

If you’re a healthcare professional interested in private markets, consider speaking with one of our financial advisors before you take the plunge. A personalized private markets investment strategy today can make a world of difference for your family’s tomorrow.