As a high-income healthcare professional, you face a unique financial journey. Years of training often mean carrying significant student debt, while your high earning potential places you in one of the steepest tax brackets. Add to that the possibility of practice ownership, liability risks, and the desire to build long-term wealth — and your financial strategy needs to do more than just “set it and forget it.”

The good news? By combining tax-smart investing, strategic asset location, and practice ownership planning, you can dramatically improve your after-tax wealth and accelerate your path to financial independence.

This guide will walk you through:

- Which investments belong in which accounts (taxable, tax-deferred, and tax-free)

- How to balance short-, medium-, and long-term goals

- How practice ownership and S-Corp elections can boost efficiency

- A sample model portfolio tailored to healthcare practitioners in their 30s

Why Tax-Smart Investing Matters for Healthcare Practitioners

Unlike many professionals, healthcare practitioners often:

- Enter their peak earning years later in life.

- Carry significant student loan balances.

- Face higher risks.

- Have the opportunity to own a practice, which adds both complexity and opportunity.

That means your investment plan must do three things at once:

- Protect your downside (insurance, emergency fund, debt management).

- Grow your wealth efficiently (smart investing + tax optimization).

- Position you for practice ownership and eventual retirement/legacy planning.

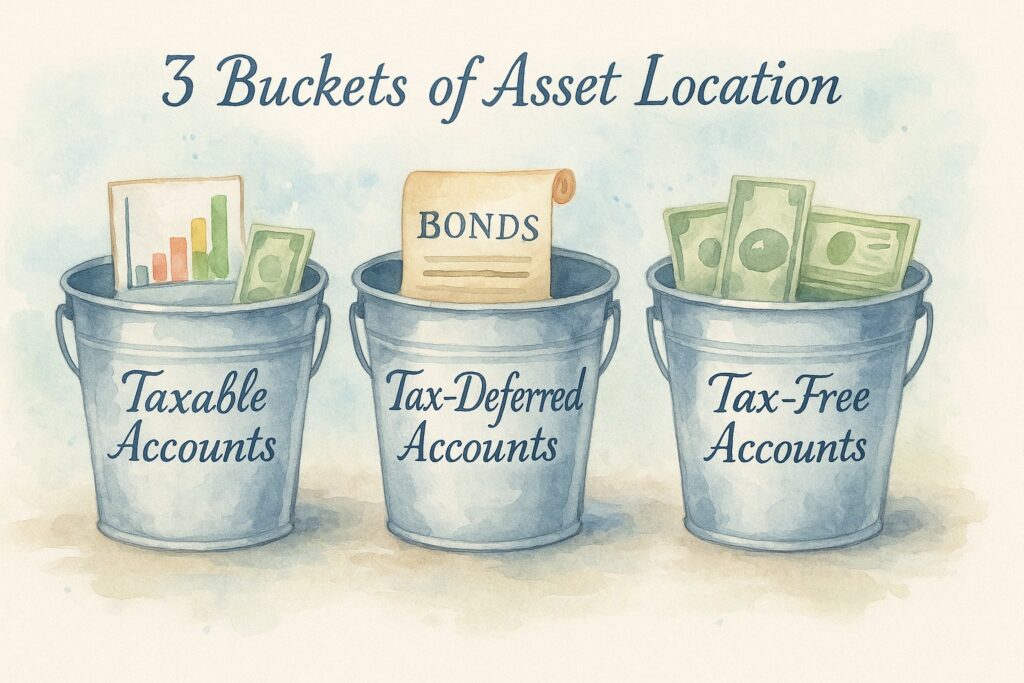

The Three Buckets of Asset Location

One of the most powerful — and overlooked — strategies is asset location: choosing the right account for the right type of investment.

Here’s the framework:

- Taxable Brokerage Accounts → Best for tax-efficient assets like ETFs and direct indexing. Also where you should keep funds earmarked for practice buy-in or other medium-term goals.

- Tax-Deferred Accounts (401k, 403b, SEP-IRA, Cash Balance Plans) → Best for income-heavy or tax-inefficient assets like bonds, REITs, and interval funds.

- Tax-Free Accounts (Roth IRA, Roth 401k, HSA) → Best for high-growth assets like small-cap equities and emerging markets.

Think of it this way:

- Growth goes in Roth (maximize tax-free compounding).

- Income goes in tax-deferred (shelter from annual taxes).

- Efficiency goes in taxable (harvest losses, benefit from long-term capital gains).

Asset Location Map for High-Income Healthcare Practitioners

| Account Type | Best Assets to Place Here | Why This Works | Time Horizon Role |

| Taxable Brokerage | – Broad-market ETFs (US & Intl) – Direct Indexing portfolios (for tax-loss harvesting) – Practice buy-in/startup fund (short-term Treasuries, CDs, money markets) | – ETFs/direct indexing are very tax-efficient – Flexibility & liquidity for medium-term goals – Capital gains taxed at lower long-term rates | Short-term: Practice fund, emergency buffer Medium-term: Wealth growth with ETFs Long-term: Tax-loss harvesting + legacy gifting |

| Tax-Deferred (401k, 403b, SEP-IRA, Cash Balance Plan) | – Bonds (Treasuries, corporates) – REITs (high income, tax-inefficient) – Interval funds (private credit, real estate, alternatives) – Target-date funds (if using employer plan) | – Shelters high-tax income assets – Defers taxes until retirement withdrawals – Ideal for income-heavy investments | Medium-term: Accelerate retirement savings Long-term: Stable income base in retirement |

| Roth IRA / Roth 401k / HSA | – Small-cap equities – Emerging markets equities – Growth-oriented ETFs – Alternatives with high growth potential | – Tax-free growth & no RMDs (Roth) – HSA = “triple tax advantage” if used for healthcare – Best place for assets with highest expected growth | Long-term: Maximize compounding, legacy planning |

| Practice Entity (S-Corp, PLLC, PC) | – Employer retirement plan (401k/profit-sharing/cash balance) – Health insurance premiums – Business overhead insurance | – Allows large tax-deductible retirement contributions – S-Corp election reduces self-employment tax – Business deductions reduce taxable income | Medium-term: Free up cash flow for practice growth Long-term: Build retirement wealth tax-efficiently |

How to Use This Map

- Think of accounts as “buckets” — put each asset in the bucket where it’s most tax-efficient.

- Rebalance annually to maintain target asset allocation without creating unnecessary taxes (use tax-advantaged accounts for most trading).

- Match goals to account liquidity:

- Short-term cash → taxable.

- Long-term growth → Roth.

- Income-producing assets → tax-deferred.

Practice Ownership and S-Corp Strategies

For many healthcare practitioners, practice ownership is both a professional milestone and a financial game-changer.

- S-Corp Election: By paying yourself a “reasonable salary” and taking the rest as distributions, you can reduce self-employment taxes.

- Retirement Plans Through Your Practice: Solo 401(k), profit-sharing, or cash balance plans allow you to shelter significant income from taxes.

- Business Deductions: Health insurance premiums, retirement contributions, and other practice-related expenses can reduce taxable income.

Done right, your practice doesn’t just generate income — it becomes one of your most powerful wealth-building tools.

Aligning Strategies with Your Timeline

Your financial goals evolve over time. Here’s how to align your strategy:

Short-Term (0–12 months)

- Build an emergency fund (3–6 months of expenses).

- Develop a student loan repayment strategy (refinance if appropriate).

- Secure risk management (disability, malpractice, umbrella insurance).

Medium-Term (2–6 years)

- Save for practice ownership or buy-in in a taxable account (liquid, low-risk assets).

- Maximize retirement contributions (401k, Roth IRA via backdoor, HSA).

- Use tax-efficient ETFs and direct indexing in taxable accounts.

Long-Term (7+ years)

- Focus on wealth growth and retirement readiness.

- Keep high-growth assets in Roth accounts for maximum compounding.

- Use tax-deferred accounts for income assets like bonds and interval funds.

- Begin legacy planning (trusts, donor-advised funds, estate planning).

A Sample Model Portfolio for a Mid-30s Practitioner

Let’s put this into practice with a sample allocation for a high-income healthcare professional in their mid-30s:

Overall Allocation

- Taxable Brokerage (30%) → liquidity + tax-efficient growth

- Tax-Deferred Accounts (40%) → retirement income & stability

- Roth IRA / Roth 401k / HSA (20%) → long-term growth engine

- Cash / Emergency Fund (10%) → safety & practice prep

1. Taxable Brokerage (30%) – Flexible, Tax-Efficient Growth

- 15% Broad-Market ETFs (US Total Market, Intl Developed)

- 10% Direct Indexing Portfolio (for tax-loss harvesting, customization)

- 5% Short-Term Treasuries / High-Yield Savings (earmarked for practice buy-in/startup fund in 5 years)

Why?

- ETFs + direct indexing = tax efficiency + loss harvesting.

- Short-term Treasuries = safe, liquid capital for practice ownership.

2. Tax-Deferred Accounts (40%) – Income & Diversification

- 20% Bonds (Treasuries + Investment Grade Corporate)

- 10% REITs / Real Estate Interval Funds (income, diversification)

- 10% Private Credit / Alternative Interval Funds

Why?

- Tax-deferred accounts are perfect for tax-inefficient, income-heavy assets.

- Interval funds provide diversification without tax drag.

3. Roth IRA / Roth 401k / HSA (20%) – High-Growth Assets

- 10% US Small-Cap Equities

- 5% Emerging Markets Equities

- 5% Growth/Innovation ETFs (tech, healthcare innovation, etc.)

Why?

- Roth = best place for highest expected growth (no tax on withdrawals).

- HSA (if available) = triple tax advantage, can double as retirement healthcare fund.

4. Cash / Emergency Fund (10%) – Safety Net

- High-Yield Savings / Money Market Fund

- Covers 3–6 months of expenses.

- Separate from practice buy-in fund.

Why?

- Protects against career/personal risk.

- Keeps you from dipping into investments during emergencies.

How This Supports Your Goals

- Short-Term (0–12 months):

- Emergency fund + short-term Treasuries = liquidity & safety.

- Student loan paydown continues alongside investing.

- Medium-Term (2–6 years):

- Taxable brokerage “practice fund” grows safely for buy-in/startup.

- Retirement savings compounding in tax-deferred & Roth accounts.

- Long-Term (7+ years):

- Roth accounts supercharge tax-free growth.

- Tax-deferred accounts provide stable retirement income.

- Taxable accounts remain flexible for wealth growth & legacy planning.

✅ This is just a starting allocation — it can be tilted more aggressive or conservative depending on your risk tolerance and timeline for practice ownership.

Bringing It All Together

For high-income healthcare practitioners, financial success isn’t just about earning more — it’s about keeping more. By:

- Matching each asset to the right account,

- Leveraging S-Corp and practice ownership strategies, and

- Aligning your investments with your timeline,

…you can build wealth more efficiently, reduce your tax burden, and set yourself up for long-term financial independence and legacy planning.

👉 Next Steps:

If you’d like a personalized review of your current portfolio and a tailored tax-smart investment plan, reach out to our team. We specialize in helping healthcare practitioners align their wealth strategies with their unique professional and personal goals.